Good afternoon!

I would like to thank the Executive Team of ECF Fellowship, Hyderabad for this humbling privilege / honour.

As I was completing my engineering course, I landed my first job at NTPC through the campus placements. The initial excitement of the monthly payday soon resulted in – “Oh! If only I could earn maybe another 20-30k more”.

A few years later, when I joined SEBI, I did get the additional pay I wished for, but it very soon again resulted in – “Oh! If only I could earn maybe another 30-40k more, I could finally be able to better manage my finances”.

When I joined my current Company a year later, I did get that additional pay again and further increments in the subsequent years as well – but only to be faced with the same challenge and the same wish every year – just a slightly bigger amount each time!

That’s when it finally dawned on me that no amount of additional pay was going to change my financial prospects unless I undertake a critical evaluation of my ‘money habits’ and initiate some required changes – in the way I manage the money I was already earning.

Around the same time, my career in the private equity industry also provided me a closer glimpse of how the ultra-rich manage, preserve and invest to grow their wealth. Hence, I ventured on to a path of exploring the various investment models / structures, tax planning, etc adopted by the rich to preserve and grow their wealth as well as on managing one’s own personal finances – gulping down any possible material available on the internet and several books on personal finance, wealth management, investments, etc in the process.

Hence, what follows is a brief summary of key learnings in this journey of trying to better manage my personal finances and hopefully set myself up on a trajectory to reach my financial goals.

To keep it better structured and concise, we will begin by introducing some basic financial terms / concepts. Fully aware that this could end up being an abstruse, humdrum talk on finance, we will not delve too much into the financial concepts but rather focus our attention on the practical aspects of these concepts.

We will then discuss some practical aspects of how to manage one’s personal finances and conclude the discussion with few action items – to hopefully nudge us to initiate some positive actions.

GUESSTIMATES

To put things to a broader perspective, let’s start by attempting the following guesstimate questions:

(Guesstimates are a favourite interview question for MBA jobs and involve trying to estimate a value or number – for which there is possibly no one correct answer. The key to attempting these questions is the logical steps through which one arrives at one’s chosen value or number)

- How much of the world’s wealth is owned by 1% of the richest population?

- How much of the world’s wealth is owned by the poorest 50% of the population?

- What would happen if the total world’s wealth is re-distributed equally to everyone?

- What are your odds of becoming a Millionaire?

- For how many generations would the world’s richest population be able to preserve their wealth?

Accordingly to a Credit Suissereport last year, 1% of the richest population owns more than half of the world’s wealth. In sharp contrast, the bottom half collectively owns less than 1% of the total wealth.

If capitalists be damned and the total wealth were to be re-distributed equally to everyone, most social scientists predict that it would only be a few years before wealth distribution inequality returns to the above highly-skewed profile.

There is some interesting research and books like ‘The Millionaire Next Door’ which have attempted to profile millionaires and compile their common characteristics. There are reports which have even gone on to the extent of trying to predict the probability of becoming a millionaire based on one’s race, education, etc.

And when it comes to preserving wealth, multiple studies suggest that 70% of wealthy families see their fortune dissipated by the third generation and 90% by the fourth. Then again, there are outliers like the Rothschild Family who have been able to preserve their vast fortune for over 200 years.

Hence, the above guesstimates seem to suggest that there is a science or an art to building and preserving wealth. And if such an art or science is learnt, there could be a possibility of not only enhancing one’s chance of becoming a millionaire but also be in a better position to preserve it much longer.

And the comforting prospect is that, if you have the patience to sift through the seemingly complicated financial concepts, investment models and structures, what lies at the core of imbibing such an art or science is this – just 5 basic financial termsand ofcourse a keen understanding of the intricate interplay between them.

We shall now introduce these key principles in the next section!

THE BASIC FINANCIAL TERMS

Attempts to improve financial reporting and corporate governance in the thousand years’ old history of private enterprise has led to a fairly standard and widely accepted financial reporting system – which is applicable equally to personal finance as well!

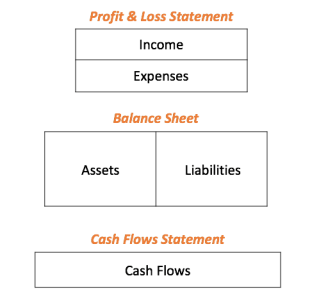

Hence, the financial health of any company today (no matter how big or small) or even that an individual, can be effectively captured using the following 5 basic financial terms:

- Income

- Expenses

- Assets

- Liabilities

- Last, but definitely not the least – ‘Cash Flows’

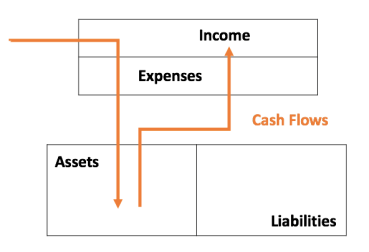

These 5 financial terms form the key heads / components of what is collectively known as financial statements– which typically includes the profit & loss statement which captures income and expenses, the balance sheet which reports the assets and liabilities and the cash flows statement which captures the cash flow activities. A highly simplified tabular representation of the financial statements is as below –

The 5 terms look rather familiar and self-explanatory, even for someone with a non-finance background.

Nevertheless, we’ll just take a quick deeper dive into two of the 5 terms – viz. ‘income’ and ‘assets’ as it would be crucial for us to better appreciate the interplay between them (and will be our focus in the next section).

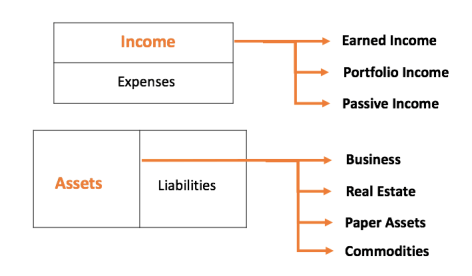

In the current financial world, income can be broadly classified into 3 categories –

- Active Income– also referred to as earned income, where ‘you have to work for your money’ (e.g. salary, commissions, etc)

- Portfolio Income– this is income from investments in stocks, bonds, etc which is better than active income, but ‘involves investment risk’ (e.g. interest, dividends, capital gains, etc)

- Passive Income– also known as cashflow income is the best form of income, where ‘your money works for you’ (e.g. rent, royalties, etc)

There are different ways in which assets have been classified for the purposes of accounting or otherwise. However, from the perspective of investments or wealth building, we will classify them into 4 broad types, as below:

- Business– owning or investing in companies which generates passive income

- Real Estate– (passive) income generating properties (residential, commercial, retail, hospitality, etc)

- Paper Assets – stocks, bonds, mutual funds, insurance, etc generating portfolio income

- Commodities – gold, silver, oil, platinum, etc generating either portfolio or passive income

Well, you may go ahead and breathe a sigh of relief – coz, that’s all we will need to take on as far as the financial concepts or terms are concerned. But, no big deal right! – just 5 basic, rather familiar and self-explanatory financial terms and a little further break down of income and assets.

We can now move on to the most important and also hopefully, the interesting part – i.e. the interplay between these financial concepts / terms from a real-life’s perspective of managing personal finance, wealth building and preservation.

THE INTER-PLAY OR CASH FLOW PATTERNS

An expression which is often used in analysing businesses and investment portfolios is “Cash is King” – rightly so, because financial history is replete with many profitable businesses which have gone kaput due to lack of cash.

Hence, we will use one of the 5 key financial terms – ‘cash flows’ to try and understand the interplay between them. For better clarity and appreciation, we will consider the cash flow pattern for 3 broad financial conditions or status. These 3 scenarios may also be viewed as the 3 stages / steps to achieving personal financial independence or freedom.

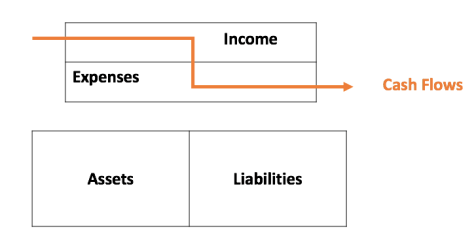

Stage 1: Poor, Jobless or Early Career (Expenses)

The first pattern typically represents the cashflows of the poor (whose condition is often referred to as ‘living from hand to mouth’) but can also be representative of someone who has just landed a job or those in their early career.

As can be seen from the diagram, the cashflows in this scenario or at this stage concerns just incomeand expenses (i.e. the profit & loss statement). Whatever income is earned or received is fully spent to meet the daily or monthly expenses. Hence, the saying – ‘the poor only have expenses’.

This cashflows pattern doesn’t involve or impact the assets and liabilities (balance sheet) of the individual.

I am sure many of us here, who have recently started working or are just a few years into a new job, can relate to this. This also explains my challenge during the early days of my career (as I mentioned in the introduction) – when my concern always was the next increment or raise in order to meet the growing expenses or financial responsibilities of transitioning from being a student to an employed.

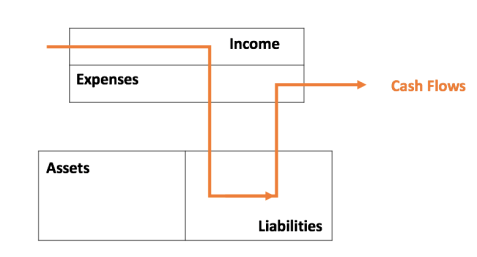

Stage 2: Middle Class (Liabilities)

The second pattern is typical of the middle-class who in an attempt to continuously upgrade lifestyle ends up acquiring more and more liabilities with every increase in pay or bonuses (often mistaking them for ‘assets’). Hence, the saying – ‘the middle-class has liabilities’.

As can be seen from the diagram above, the cashflows, therefore, starts impacting the liabilitiesside of the balance sheet – i.e. the extra income (over and above the regular monthly expenses) is now being used to generate liabilities(car loans, home loans, personal loans, credit cards, etc). These new liabilities then keep piling on to the expenses – in form of EMIs, maintenance, insurance costs, interest payments, etc.

Again, I am sure many of us here, particularly those who are already several years into a working career can relate to this. If so, many of us would also be already aware of the risk of over-indulgence and incessant loading of liabilities – which can easily lead one into the typical middle-class debt trap.

Hence, its critical to know and appreciate the difference between ‘assets’ and ‘liabilities’ which is succinctly put by Robert Kiyosaki in his top selling book “Rich Dad, Poor Dad” as – an asset puts money in your pocket; a liability takes money out of your pocket.

For example, the brand new car you just bought is a liability and not an asset – as it takes money out of your pocket for fuel, maintenance, repairs, insurance, etc (unless ofcourse you give it to a car renting company like Ola or Uber and are able to earn excess income – in which case, it is an asset as it would put money into your pocket). Similarly, your house, although for accounting purposes maybe considered an asset, is actually a liability as it takes money out of your pocket in the form of the monthly EMIs (unless ofcourse you buy a house or commercial space for renting and are able to earn extra income).

This critical understanding is what separates the rich from the middle class or the poor, who acquire assets (not liabilities), as we shall see in the next cashflows pattern below.

Stage 3: The Rich (Assets)

The above pattern represents the cash flows of the rich – who as highlighted earlier, uses their surplus income to acquire assets. Over time, the assets column generates enough income to cover the regular expenses. The excess income can then be continuously reinvested into more assets, generating even more income. Hence, the saying – ‘the rich get richer!”

If you manage to reach this stage and achieve the above virtuous cycle, you don’t even have to worry about money or losing your job – because unlike the poor or the middle-class, whose cashflow pattern requires them to work for money, the rich can manage their cash flow pattern to have their money work for them.

PERSONAL FINANCE

Everyone’s financial goal or dream is to achieve the cashflows pattern of the rich – to generate wealth and then hopefully preserve them for as long as possible. The first step towards accomplishing that goal and graduating from the cashflows pattern of the poor to that of the rich is – effective personal finance management.

Personal finance involves effectively managing one’s INCOME and EXPENSES to generate enough SAVINGS, to use it to make INVESTMENTS to grow one’s wealth and then PROTECT or guard them from any unforeseen or adverse events.

The different aspects of personal finance (capitalised terms above) each deserves a separate session. But we will focus our discussion today on the most critical and ofcourse the starting point of any personal finance management – i.e. allocation of one’s income. Personal finance management cannot get a kick-start without some surplus cashflows being generated though an effective budgeting or allocation of one’s income.

Given that this a fundamental concept, there are many opinions and suggestions on this topic. One simplified and general budgeting rule is the 50:30:20 (FiftyThirtyTwenty) rule popularised by Senator Elizabeth Warren in her book – All Your Worth: The Ultimate Lifetime Money Plan.

Accordingly to this thumb-rule – 50% of the earnings after tax should be used towards necessities, 30% of the money should be spent on luxuries or wants / desires and the balance 20% should be saved and invested towards achieving one’s financial goals.

Evidently, there is no ‘one size fits all’ and the allocations could vary depending on income levels, personal lifestyle preferences, timelines set for achieving certain personal financial goals, etc. Hence, I would like to present for our consideration a more detailed suggested income allocation pattern – particularly for those in the early years of a career.

Let’s delve a little deeper into the reasoning behind the suggested allocation above and the required changes as one progresses in his / her career –

- Necessity– At the start of a career, income is low. Hence, expenses on necessities like rent, food, clothing, etc is high as a percentage. This percentage share should come down with increase in income.

- Learning– At the start of one’s career, investing in oneself or allocation towards learning is an important consideration – to enhance or develop new skills for generating higher and possibly, multiple incomes.

- Emergency– This is important to take care of any form of emergencies – medical, job change, etc and to avoid taking on high-cost debts due to such unfortunate incidents. This allocation may not be required after a sizable fund has been set aside – except to enhance the amount commensurate to the lifestyle upgrades.

- Fun– The idea here is to pre-allocate or budget for such fun related activities so that you can enjoy them fully and guilty-free.

- Investment– It’s important that the habit of saving and investing is developed right from the start (no matter how small) and to increase this critical allocation as one’s income grows.

Persistent achievement of an allocation along the above suggested lines would help set up a strong foundation to effectively managing one’s personal finances to achieve the cashflows pattern of the rich and attain one’s financial goals.

ACTION POINTS / CONCLUSION

As evident from the discussion today, personal finance as a concept is a very basic. However, the more critical and challenging part is initiating the required changes / actions.

Therefore, I would like to conclude the deliberations today with 3 action items to hopefully nudge us towards initiating atleast the first few critical baby steps –

- Action Item 1: Monthly Expenses Review– In my own experience, a review of one’s monthly expenses is the best place to start. Initiating this habit itself is enough to effect some positive changes in one’s spending / money habits.

- Action Item 2: Savings / Investments– As already highlighted earlier, it’s all about the habit. Therefore, let’s target to start allocating atleast 10% our monthly net income towards savings / investments.

- Action Item 3: Reinforcement– Once we have initiated the above two changes, a regular reinforcement would be critical to sustain the momentum. Nothing works better than a regular consumption of materials related to finance / personal finance.

It’s often hard to pick from the many good options available – but my suggestion would be to start with reading atleast these 2 books – ‘The Richest Man in Babylon” (by George S Clason) and “Rich Dad Poor Dad” (by Robert T Kiyosaki).

Thank you all once again!

Thank you for this great content. I think this article will complement it pretty well

https://edulers.co/how-to-build-wealth/

LikeLike